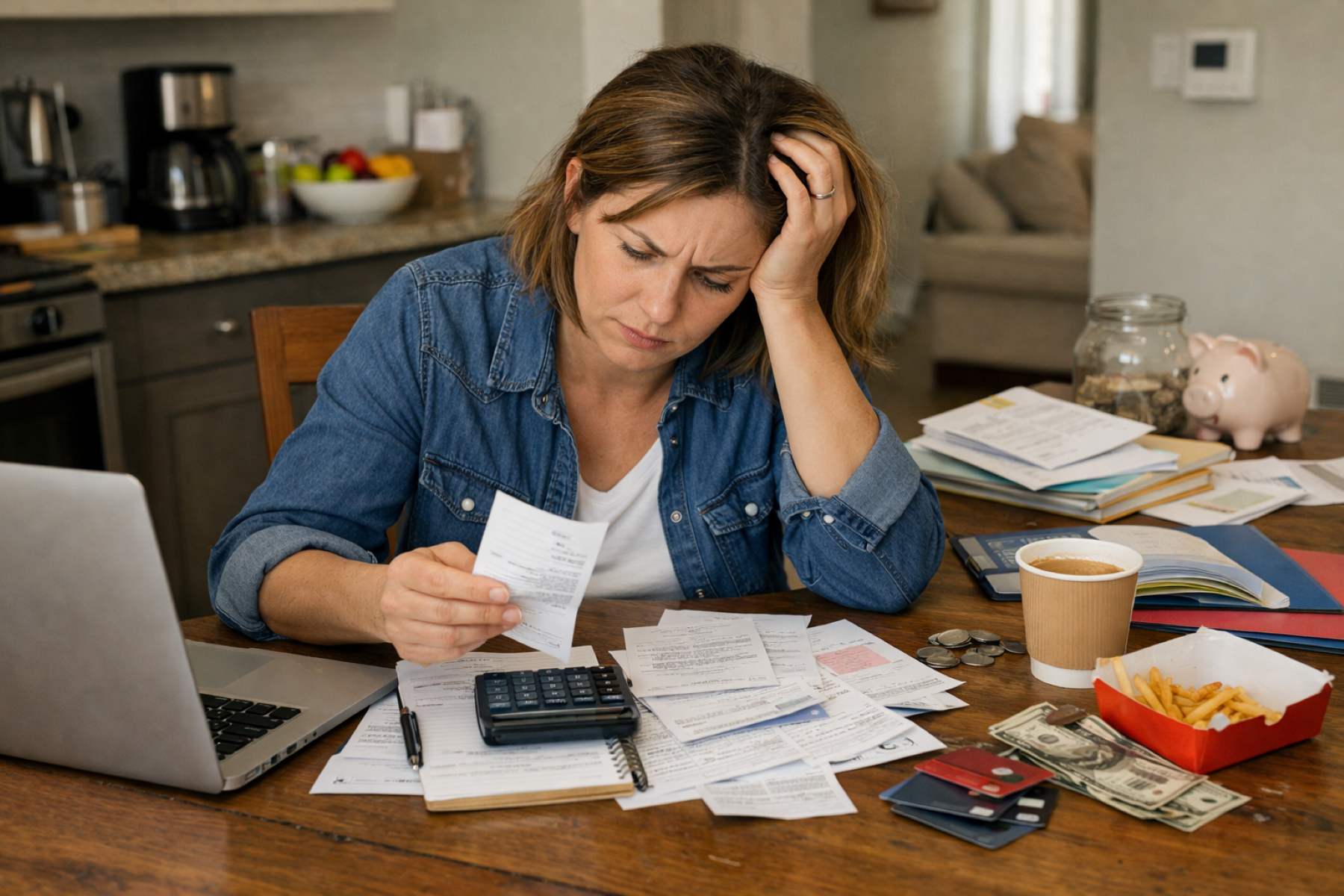

Managing money often feels like trying to fill a bucket that has a few tiny, invisible holes at the bottom. You pour in your hard-earned salary, confident that you have enough to last the month, only to find the container nearly empty before the next paycheck arrives. This phenomenon is often the result of personal budget inefficiency, a common hurdle that even the most disciplined savers face. It isn’t usually the “big” purchases that sink the ship, but rather the subtle, overlooked leaks in our financial planning that go unnoticed until the damage is done.

Understanding Personal Budget Inefficiency

Before we dive into the specific pitfalls, it is helpful to define what we mean by this concept. In simple terms, it refers to a breakdown in the flow of your finances where your actual spending doesn’t align with your intended goals. This inefficiency occurs when a budget looks perfect on paper—or on a spreadsheet—but fails to account for the messy, unpredictable nature of real life. When your financial plan is inefficient, you aren’t just losing money; you are losing the peace of mind and the long-term security that a healthy savings account provides.

1. Neglecting the Small Daily Recurring Expenses

One of the most frequent contributors to personal budget inefficiency is the dismissal of “micro-transactions.” We often tell ourselves that a five-dollar coffee or a small digital app upgrade won’t move the needle on our financial health. However, these small daily habits have a cumulative effect that can be startling when viewed over the course of a year.

When we omit these items from our budget, we create a false sense of surplus. By the time the end of the month rolls around, that “extra” money has vanished into a dozen different small purchases. To fix this, it is helpful to track every cent for at least thirty days. You might find that your morning routine is costing you more than your monthly car insurance.

2. Failing to Establish Emergency Funds

A budget without an emergency fund isn’t actually a plan; it is a best-case scenario. Many people build their budgets assuming that every month will be a standard, “average” month. Unfortunately, life rarely cooperates with our spreadsheets. When a tire blows out or a home appliance breaks, people without an emergency fund are forced to dip into money reserved for rent or groceries.

This creates a cycle of debt that is difficult to break. Integrating an emergency fund contribution as a “fixed expense” in your budget is essential. Without this buffer, one bad afternoon can derail months of progress and lead to significant personal budget inefficiency.

3. Underestimating Variable Utility Bill Costs

It is easy to budget for a fixed rent payment or a car loan because the number never changes. Utilities, however, are a different story. Many people make the mistake of budgeting based on their lowest monthly bill, such as a mild spring month when neither the heater nor the air conditioner is running.

When the peak of summer or winter hits, those bills can double, leaving a massive hole in the budget. A more effective strategy is to look at your utility costs over an entire year and calculate the average. By setting aside that average amount every month, you build a small surplus during the “cheap” months that covers the spike during the expensive ones.

4. Mixing Personal and Professional Finances

For freelancers, side-hustlers, or small business owners, the line between personal and professional spending can become incredibly blurry. Using the same bank account for business expenses and grocery shopping is a recipe for personal budget inefficiency. It makes it nearly impossible to see how much profit you are actually making and, more importantly, how much you are personally spending.

When these funds are mixed, you might feel wealthier than you are because the business revenue is sitting in your checking account. This often leads to overspending on personal items using money that should have been reserved for taxes or business reinvestment.

5. Setting Unrealistic Restrictive Spending Goals

There is a common temptation to “slash and burn” a budget when we first decide to get serious about saving. We tell ourselves we will never eat out again or that we will cancel every entertainment subscription. While the intention is noble, overly restrictive goals are rarely sustainable.

Psychologically, if a budget feels like a punishment, you are much more likely to abandon it entirely after a few weeks. This “rebound” spending often results in a larger financial loss than if you had just allowed for a small, reasonable “fun” category. A successful budget should feel like a set of guardrails, not a cage.

6. Ignoring the Impact of Inflation on Groceries

In recent years, many households have noticed that the same amount of money buys significantly less at the supermarket. If you are still using a grocery budget from two or three years ago, you are likely experiencing personal budget inefficiency. Inflation is a silent budget-killer that requires constant monitoring and adjustment.

Periodically reviewing your receipts and adjusting your food budget to reflect current market prices is vital. It allows you to make informed decisions, such as switching to generic brands or planning meals around sales, rather than being surprised at the checkout counter.

7. Omitting Occasional Annual Subscription Fees

The “set it and forget it” nature of modern subscriptions is a double-edged sword. While convenient, annual fees for software, gym memberships, or warehouse clubs often catch us off guard. Because they only happen once a year, they are frequently left out of monthly budget calculations.

When a hundred-dollar annual fee suddenly hits your account, it can throw your entire month out of balance. The most effective way to handle these is to list every annual fee you pay and divide the total by twelve. This ensures that when the bill arrives, the money is already waiting, preventing any sudden personal budget inefficiency.

Achieving financial stability isn’t about perfection; it’s about awareness. Addressing personal budget inefficiency requires a shift in perspective—viewing your budget as a living document that needs regular check-ups and honest adjustments. By identifying these seven common leaks, you can move from a state of financial stress to one of empowerment.

Remember, the goal of a budget is to give you the freedom to spend on what truly matters to you without the guilt or the mid-month panic. It is about making sure that every dollar you earn is working as hard as you do.